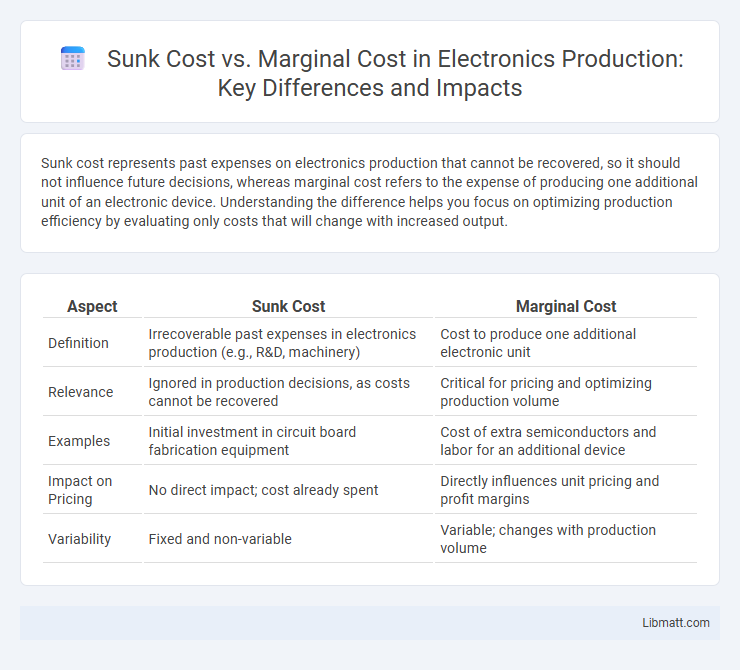

Sunk cost represents past expenses on electronics production that cannot be recovered, so it should not influence future decisions, whereas marginal cost refers to the expense of producing one additional unit of an electronic device. Understanding the difference helps you focus on optimizing production efficiency by evaluating only costs that will change with increased output.

Table of Comparison

| Aspect | Sunk Cost | Marginal Cost |

|---|---|---|

| Definition | Irrecoverable past expenses in electronics production (e.g., R&D, machinery) | Cost to produce one additional electronic unit |

| Relevance | Ignored in production decisions, as costs cannot be recovered | Critical for pricing and optimizing production volume |

| Examples | Initial investment in circuit board fabrication equipment | Cost of extra semiconductors and labor for an additional device |

| Impact on Pricing | No direct impact; cost already spent | Directly influences unit pricing and profit margins |

| Variability | Fixed and non-variable | Variable; changes with production volume |

Introduction to Sunk Cost and Marginal Cost in Electronics Production

Sunk cost in electronics production refers to past expenses on materials, equipment, or design that cannot be recovered, such as initial R&D investment or outdated component procurement. Marginal cost represents the additional expense incurred when producing one more unit of an electronic product, including materials, labor, and energy costs. Understanding these concepts helps your manufacturing decisions by focusing on future costs rather than irrecoverable past expenditures.

Defining Sunk Cost in Electronics Manufacturing

Sunk cost in electronics manufacturing refers to the expenses already incurred on production equipment, research, and development that cannot be recovered regardless of future decisions. These costs, such as investments in specialized machinery or prototype development, should not influence your decisions about scaling production or shifting to new technologies. Understanding sunk costs helps optimize resource allocation by focusing on marginal costs--the additional cost of producing one more unit--rather than past investments.

Understanding Marginal Cost in Electronic Product Production

Marginal cost in electronic product production refers to the expense incurred when manufacturing one additional unit, encompassing materials, labor, and variable overheads. Unlike sunk costs, which are past investments like research and development that cannot be recovered, marginal costs directly influence your decisions on scaling production. Accurately calculating marginal cost helps optimize pricing strategies and maximize profitability in electronic manufacturing.

Key Differences Between Sunk Cost and Marginal Cost

Sunk cost in electronics production refers to past expenses such as specialized equipment or research that cannot be recovered, whereas marginal cost involves the expense of producing one additional unit, including materials and labor. Understanding this distinction helps you make informed decisions by ignoring sunk costs and focusing on marginal costs for future production efficiency. Marginal cost is crucial for optimizing output levels and pricing strategies, while sunk cost should not influence current or future production choices.

Real-World Examples: Sunk Costs in Electronics Factories

Sunk costs in electronics factories include expenses such as the purchase of specialized machinery and factory setup costs that cannot be recovered once incurred. Marginal cost, on the other hand, refers to the expense of producing one additional unit of electronics, primarily influenced by raw materials like semiconductors and labor hours. Understanding these distinctions helps electronics manufacturers make informed decisions about scaling production and avoiding losses from irreversible investments.

Marginal Cost Calculations in PCB and Component Assembly

Marginal cost calculations in PCB and component assembly focus on the additional expense incurred for producing one more unit, including materials and labor specific to the extra unit. Sunk costs, such as initial design and setup fees for printed circuit boards, are excluded since they do not change with production volume. Understanding marginal cost helps optimize production efficiency and pricing strategies by highlighting the incremental cost impact of each additional electronic assembly unit.

Impact of Sunk Cost on Production Decision-Making

Sunk costs in electronics production, such as investments in outdated machinery or non-recoverable R&D expenses, do not influence marginal cost calculations and should not affect current production decisions. Your focus should remain on marginal cost, which represents the expense of producing one additional unit and directly impacts pricing and output level choices. Ignoring sunk costs ensures more efficient resource allocation and prevents financial losses in manufacturing processes.

Marginal Cost Analysis for Optimizing Electronics Output

Marginal cost analysis in electronics production focuses on the additional cost incurred for producing one more unit of a device, helping identify the most cost-effective output level. Sunk costs, such as initial machinery investments, are excluded since they are irrecoverable and do not affect current production decisions. By evaluating marginal costs, you can optimize production volume to maximize profit while minimizing unnecessary expenditure on excess units.

Sunk Cost Fallacy and Its Effects in Electronics Businesses

Sunk cost fallacy in electronics businesses leads companies to continue investing in outdated or unprofitable technologies due to past expenditures rather than current marginal costs. Ignoring marginal cost--which reflects the expense of producing one additional unit--results in inefficient resource allocation and reduced competitiveness in rapidly evolving markets. Recognizing the irrelevance of sunk costs enables electronic firms to pivot toward cost-effective production decisions and innovation strategies.

Strategic Recommendations: Managing Costs in Electronics Production

Prioritize marginal cost analysis over sunk costs to optimize production efficiency in electronics manufacturing, ensuring decisions reflect current and future expenses rather than past investments. Implement flexible production processes and adopt just-in-time inventory systems to minimize marginal costs and respond swiftly to market demand changes. Your strategic approach should focus on continuous cost evaluation and adjustment to maintain competitiveness and profitability in the electronics industry.

Sunk Cost vs Marginal Cost (production electronics) Infographic