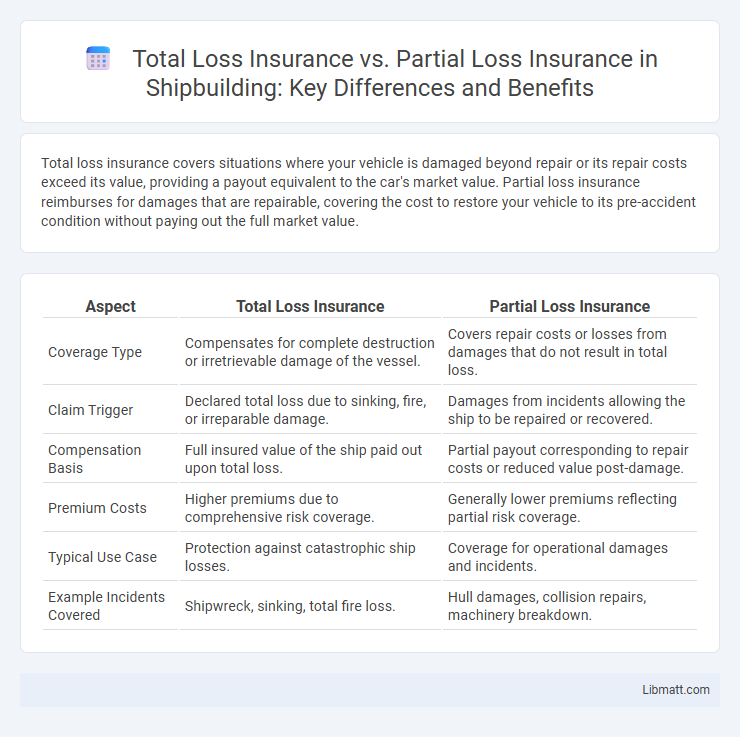

Total loss insurance covers situations where your vehicle is damaged beyond repair or its repair costs exceed its value, providing a payout equivalent to the car's market value. Partial loss insurance reimburses for damages that are repairable, covering the cost to restore your vehicle to its pre-accident condition without paying out the full market value.

Table of Comparison

| Aspect | Total Loss Insurance | Partial Loss Insurance |

|---|---|---|

| Coverage Type | Compensates for complete destruction or irretrievable damage of the vessel. | Covers repair costs or losses from damages that do not result in total loss. |

| Claim Trigger | Declared total loss due to sinking, fire, or irreparable damage. | Damages from incidents allowing the ship to be repaired or recovered. |

| Compensation Basis | Full insured value of the ship paid out upon total loss. | Partial payout corresponding to repair costs or reduced value post-damage. |

| Premium Costs | Higher premiums due to comprehensive risk coverage. | Generally lower premiums reflecting partial risk coverage. |

| Typical Use Case | Protection against catastrophic ship losses. | Coverage for operational damages and incidents. |

| Example Incidents Covered | Shipwreck, sinking, total fire loss. | Hull damages, collision repairs, machinery breakdown. |

Introduction to Total Loss and Partial Loss Insurance

Total loss insurance covers damages when a vehicle is deemed completely irreparable or the repair cost exceeds its market value, ensuring full compensation up to the insured value. Partial loss insurance applies when damages are repairable, covering repair costs without surpassing the vehicle's actual cash value. These insurance types define claim processes based on the extent of damage and financial thresholds established by insurers.

Definition of Total Loss Insurance

Total Loss Insurance provides coverage when your vehicle is damaged beyond repair or its repair costs exceed a predetermined percentage of its value, often around 70-80%. This type of insurance compensates you for the actual cash value of your vehicle before the loss, rather than covering repair expenses. It ensures financial protection in scenarios where the vehicle is considered a total loss by the insurance company.

Definition of Partial Loss Insurance

Partial loss insurance covers damages to insured property that do not exceed the total value, allowing for repairs instead of a full replacement. It provides compensation proportional to the extent of damage, unlike total loss insurance, which applies when the cost to repair exceeds the asset's value. This type of coverage is common in auto and property insurance policies, protecting policyholders from partial damage claims.

Key Differences Between Total Loss and Partial Loss Insurance

Total loss insurance covers situations where your vehicle or property is damaged beyond repair or the cost to restore exceeds its value, resulting in a full payout based on the item's market worth. Partial loss insurance applies when damage is repairable, and compensation covers the repair expenses rather than the entire value. Your choice between these types affects claim settlement, premium costs, and coverage scope, highlighting the importance of understanding the distinction for effective financial protection.

Coverage Scope: What Each Policy Protects

Total loss insurance covers the full replacement or actual cash value of your vehicle when it is completely destroyed or stolen, ensuring maximum financial protection. Partial loss insurance, on the other hand, provides coverage for repairs or damages that do not exceed the total loss threshold, such as collision repairs or minor accidents. Understanding the coverage scope helps you choose the right policy based on how much risk you are willing to bear for different types of vehicle damage.

Claim Process Comparison

Total loss insurance claims typically involve a straightforward evaluation where the insurer deems the vehicle repair costs exceed its actual cash value, resulting in a lump-sum payout based on the car's market worth before the damage. Partial loss insurance claims require detailed assessments to estimate repair expenses and determine the coverage amount for damages that do not render the vehicle a total loss. Understanding the distinctions in your claim process helps ensure timely settlements and proper documentation tailored to each insurance type.

Factors Affecting Insurance Payouts

Factors affecting insurance payouts include the extent of vehicle damage, with total loss insurance covering situations where repair costs exceed the vehicle's value, while partial loss insurance applies to damages that are repairable at a lower cost. Insurance policy terms, such as deductibles, coverage limits, and depreciation, also influence the payout amount. Understanding these factors helps you evaluate and maximize your claim based on the type of loss your vehicle sustains.

Pros and Cons of Total Loss Insurance

Total loss insurance offers the advantage of comprehensive financial protection by covering the full replacement cost of a vehicle when repair expenses exceed its value, ensuring policyholders are not burdened with significant out-of-pocket costs. However, the cons include generally higher premiums compared to partial loss insurance and the potential for claims disputes during vehicle valuation processes. This type of insurance is ideal for new or high-value vehicles but may not be cost-effective for older vehicles with lower market value.

Pros and Cons of Partial Loss Insurance

Partial loss insurance covers damages to your vehicle that are repairable, offering lower premiums compared to total loss insurance. It allows you to recover repair costs without the total vehicle replacement, but may result in higher out-of-pocket expenses if repairs exceed coverage limits. Your choice depends on vehicle value, risk tolerance, and budget for potential repairs.

Choosing the Right Insurance for Your Needs

Total loss insurance provides full compensation when a vehicle is irreparably damaged or stolen, while partial loss insurance covers repairs for damages that do not exceed the vehicle's value. Selecting the right policy depends on factors such as the vehicle's age, value, and your financial ability to cover deductibles or replacement costs. Understanding coverage limits and claim processes ensures optimal protection aligned with your budget and risk tolerance.

Total loss insurance vs partial loss insurance Infographic